Just how much are you paying for no-fault coverage, anyway? Check your declarations sheet

Compared to other coverages, the cost of no-fault coverage might not be as high as you think – how does this impact arguments that the cost of no-fault insurance in Michigan is out of control?

The cost of no-fault insurance in Michigan has been a significant subject in debates to reform the system. Michigan SB 248, now with a substitute version awaiting a vote by the House, allegedly aims to decrease the cost of no-fault; however, what supporters of the bill fail to mention is that in exchange for cheaper auto insurance, people in this state, especially those who suffer severe, traumatic injury resulting from car accidents, will lose access to the high quality care our no-fault system is known for, among other benefits – all for a two-year, $100 per vehicle reduction on premiums. After those two years, no further savings are guaranteed while the cuts to the quality of care and access to that care will remain.

During the no-fault “reform” debates taking place as SB 248 is being contemplated, the discussions concerning the cost of auto no-fault insurance in Michigan beg the question: just how much are you paying for it? The best answer to this question doesn’t come from news coverage about this subject. It’s not within the text of the no-fault law. You can answer it by looking at your insurance declaration sheet.

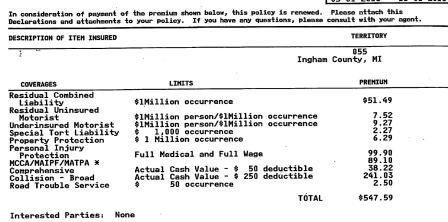

Let’s use this declaration sheet for an auto insurance policy issued by Home-Owners Insurance Company as an example. The coverages and premium amounts are as follows:

- Residual Combined Liability ($1 million occurrence) – $51.49

- Residual Uninsured Motorist ($1 million person/$1 million occurrence) – $7.52

- Underinsured Motorist ($1 million person/ $1 million occurrence) – $9.27

- Special Tort Liability ($1,000 occurrence) – $2.27

- Property Protection ($1 million occurrence) – $6.29

- Personal Injury Protection (Full medical and Full Wage) – $99.90

- MCCA/MAIPF/MATPA – $89.10

- Comprehensive (actual cash value – $40 deductible) – $38.22

- Collision – Broad (actual cash value – $250 deductible) – $241.03

- Road Trouble Service ($50 occurrence) – $2.50

Which premium is the highest for this consumer? Collision coverage – not no-fault coverage ($241.03 vs. $99.90)!

Is the same true in your case? Take a look at your own auto insurance declaration sheet and figure out what costs you the most. Is it your no-fault coverage, or something else? If it’s not your no-fault coverage, does it call into question all of these claims that Michigan’s unlimited medical coverage under auto no-fault law is driving costs of out control, and thus our system needs to be “reformed”?

Let us know what you find.